FX Week Ahead Overview:

- The final week of January sees an economic calendar supersaturated with ‘high’ rated event risk.

- Inflation data due from Australia and New Zealand may help the Aussie and the Kiwi decouple from broader risk-off trends.

- While the Bank of Canada also meets on Wednesday, the only central bank that anyone really wants to hear from is the Federal Reserve.

For the full week ahead, please visit the DailyFX Economic Calendar.

01/25TUESDAY | 00:30 GMT | AUD INFLATION RATE (4Q)

According to a Bloomberg News survey, 4Q’21 Australia inflation rates (CPI) increased by +3.2% y/y from +3% y/y. While these inflation rates are nowhere close to those being experienced among other developed economies, the Reserve Bank of Australia’s target range is +1-3%, suggesting that price pressures will still be above the upper band. Although the RBA has embraced a ‘lower for longer’ policy – reducing QE but keeping QE going until February 2022 – pressure will continue to build for a reduction in stimulus in the coming months, providing a cushion for the Australian Dollar.

01/26 WEDNESDAY | 15:00 GMT | CAD BANK OF CANADA RATE DECISION

The Bank of Canada meets for the first time in 2022 this week, with more information about the COVID-19 omicron variant and its impact on the global economy in hand. Accordingly, the BOC is likely to be emboldened in its thought process outlined last month, when policymakers more or less downplayed the impact of omicron on the path of interest rates in 2022. Rates markets have taken notice and have taken a more aggressive stance in recent weeks.

In mid-December, Canada overnight swaps were pricing in a 50% chance of the first 25-bps rate hike arriving in March 2022. The limited impact of omicron plus the surge in oil prices – energy accounts for approximately 11% of Canadian GDP – has seen traders boost their bets that the BOC will act more aggressively in the first half of 2022. There is now a 102% chance of a 25-bps rate hike in March (100% chance of a 25-bps rate hike plus a 2% chance of a 50-bps rate hike), while the second 25-bps hike is likely to arrive in April (84% chance) and a third 25-bps hike is discounted for June (62% chance).

01/26 WEDNESDAY | 19:00 GMT | USD FEDERAL RESERVE RATE DECISION & PRESS CONFERENCE

The Federal Reserve has a tricky task ahead of it this week when it meets for the first time in 2022. Global financial markets have been upended by concerns that the FOMC will aggressively tighten policy this year – even though much of the concern has appeared during the communications blackout window ahead of the January policy meeting.

There are 156.75-bps of rate hikes discounted through the end of 2023 while the 2s5s10s butterfly is just off of its widest spread since the Fed taper talk began in June. Ahead of the January Fed meeting, rates markets are effectively pricing in a 100% chance of six 25-bps rate hikes and a 27% chance of seven 25-bps rate hikes through the end of next year. Furthermore, expectations for a 50-bps rate hike to start the hike cycle have edged higher in recent weeks.

01/26 WEDNESDAY | 21:45 GMT | NZD INFLATION RATE (4Q)

According to a Bloomberg News survey, price pressures in New Zealand continue to ratchet higher as 2021 came to a close. Consensus forecasts point to headline inflation (CPI) reaching +5.7% y/y in 4Q’21, up from +4.9% y/y in 3Q’21. While the data suggest that the Reserve Bank of New Zealand will act aggressively in the coming months to tighten policy, those expectations have already been priced-in by markets: the RBNZ is forecast to raises rates by 25-bps at all but one meeting this year. A strong inflation reading may not provide the New Zealand Dollar the reprieve it desperately needs.

01/27 THURSDAY | 13:30 GMT | USD Gross Domestic Product (4Q A)

The US economy appears to have slowed down in the final weeks of 2021, but not so much as to upend what was an otherwise strong quarter for growth. The COVID-19 omicron variant created a chilling effect on business activity and travel, sending expected 4Q’21 US GDP from near +10% annualized to roughly half that by the time the quarter came to a close; according to a Bloomberg News survey, a reading of +5.5% annualized is expected.

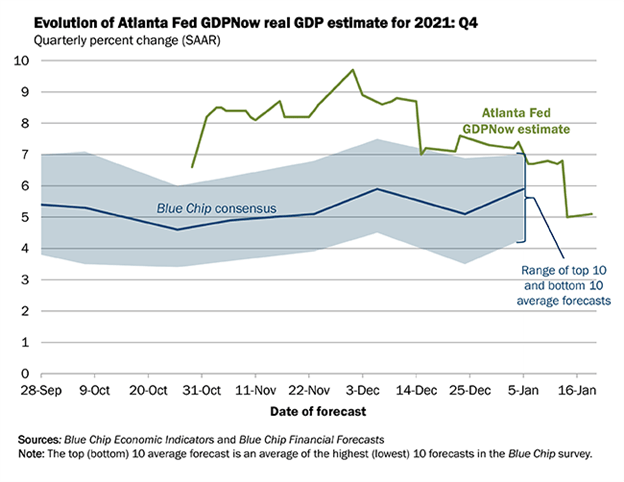

ATLANTA FED GDPNOW: 4Q’21 GROWTH ESTIMATE (JANUARY 19, 2022) (Chart 1)

Based on the data received thus far about 4Q’21, the Atlanta Fed GDPNow growth forecast is now at +5.1% annualized, up from +5% on January 14. The upgrade was a result of “the nowcast of fourth-quarter real gross private domestic investment growth increased from +18.1% to +18.6%.”

The final update to the 4Q’21 Atlanta Fed GDPNow growth forecast is due on Wednesday, January 26 after the December US goods trade balance and December US new home sales figures are released.

— Written by Christopher Vecchio, CFA, Senior Strategist

Read More:FX Week Ahead – Top 5 Events: Australia & New Zealand Inflation Rates; BOC & Fed Meetings; US GDP

2022-01-24 17:45:25