necati bahadir bermek

With the rapid growth in funding ratios over the past year, an increasing number of UK-defined benefit (DB) pension schemes have been contemplating their investment approach for the endgame – the point at which a plan moves from being underfunded to being fully funded or even having a surplus.

Our analysis suggests that gold is an effective addition to a DB portfolio, helping a plan achieve its desired endgame by:

- contributing to long-term growth, and

- providing diversification that helps reduce funding level volatility.

How have UK DB pension schemes fared recently?

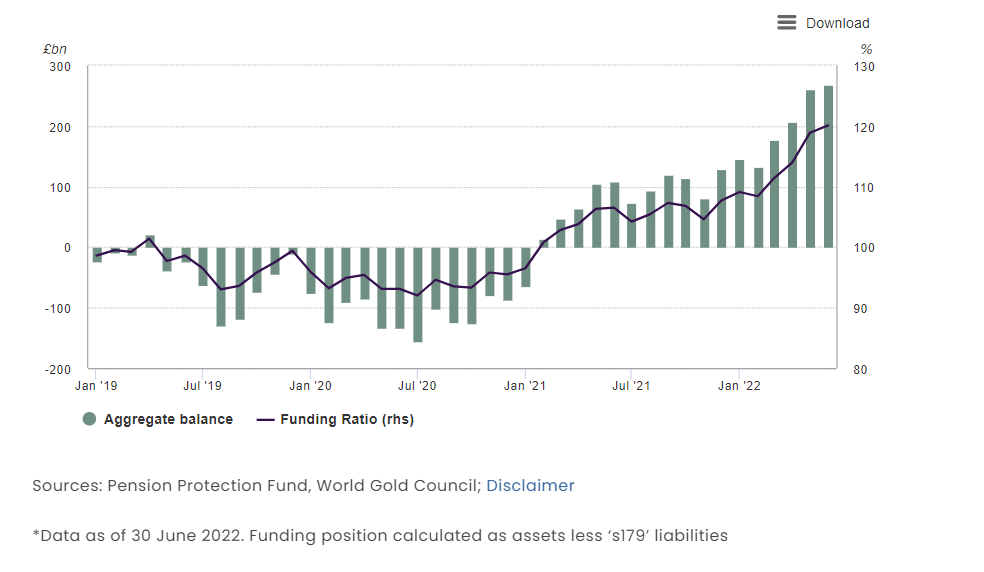

To answer that question, we examine the evolution of the PPF 7800 index published by the Pension Protection Fund (PPF) since 2019. The index indicates the estimated funding position for the DB pension schemes in the PPF’s eligible universe and is based upon compensation paid by the PPF, which may be lower than full scheme benefits. At the end of 2019, the aggregate scheme funding ratio (the ratio of a scheme’s total assets to liabilities) was 99.4%.

In the first half of 2020, one immediate consequence of the COVID-19-induced crisis is that yields collapsed, along with equity markets. Together, these two developments were challenging for UK DB pensions (Chart 1). With the present value of liabilities rising and asset values falling, aggregate DB schemes’ deficits widened to lows of 92% by July 2020.

Chart 1: COVID-19 created significant challenges for UK DB pensions

Historical aggregate funding position and funding ratio of schemes in the PPF universe*

Since then, funding levels have steadily risen. Strong returns from growth assets were a key driver of the large improvements in scheme funding levels over 2021, with global equity markets reaching new highs following a strong economic recovery across the globe.

More recently, for a traditional DB plan, particularly a closed plan, a higher yield curve – commensurate with rising inflation – has provided a further welcome tailwind by decreasing the present value of liabilities.

At the end of June, the PPF 7800 index shows funding levels were at 120%, levels not seen in a decade. And while disaggregating the data reveals that there is significant dispersion in the funding ratios among schemes, it is important for DB plans to seek to maintain the funding status gains made over the past year. This is especially so, as worries surrounding the global economic environment continue to mount and growth-oriented assets remain under pressure.

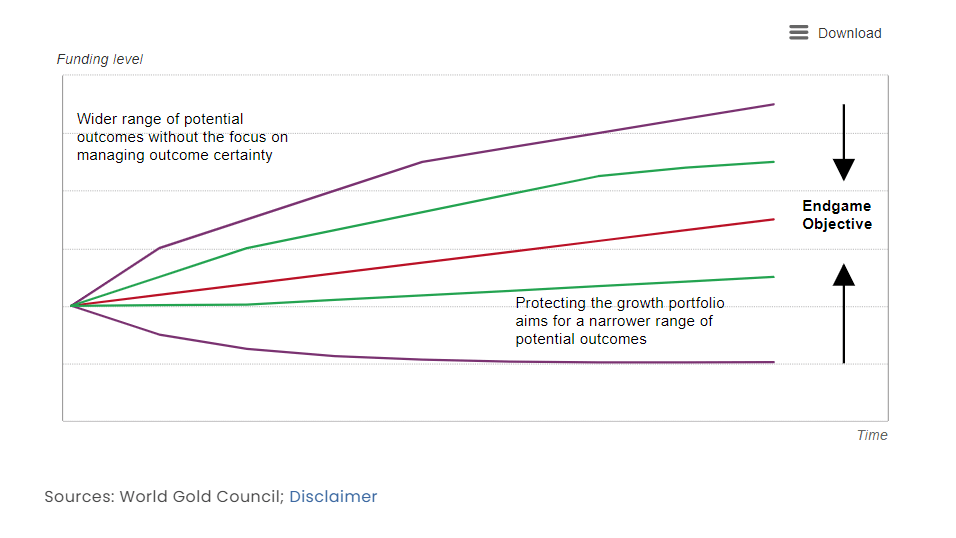

Managing outcome certainty

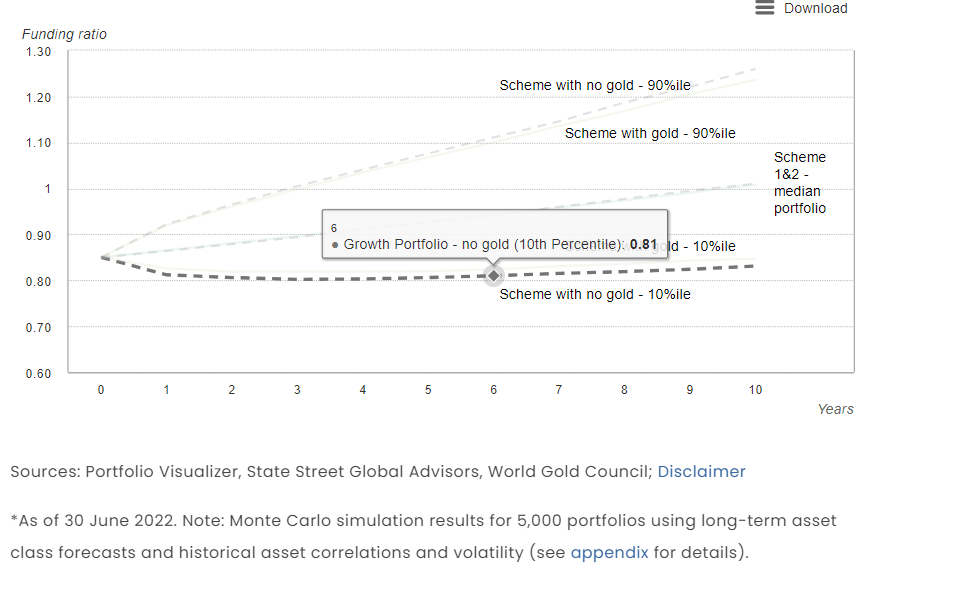

Taking into consideration recent improvements in the funding status of UK pension schemes and the breadth of macroeconomic challenges, we believe DB schemes should consider ways to protect their growth portfolio and narrow the range of potential outcomes. This would increase the likelihood of achieving their chosen endgame (Chart 2).

Chart 2: Pension schemes should seek to increase the certainty of achieving their endgame

Hypothetical development of DB funding levels based on different strategies

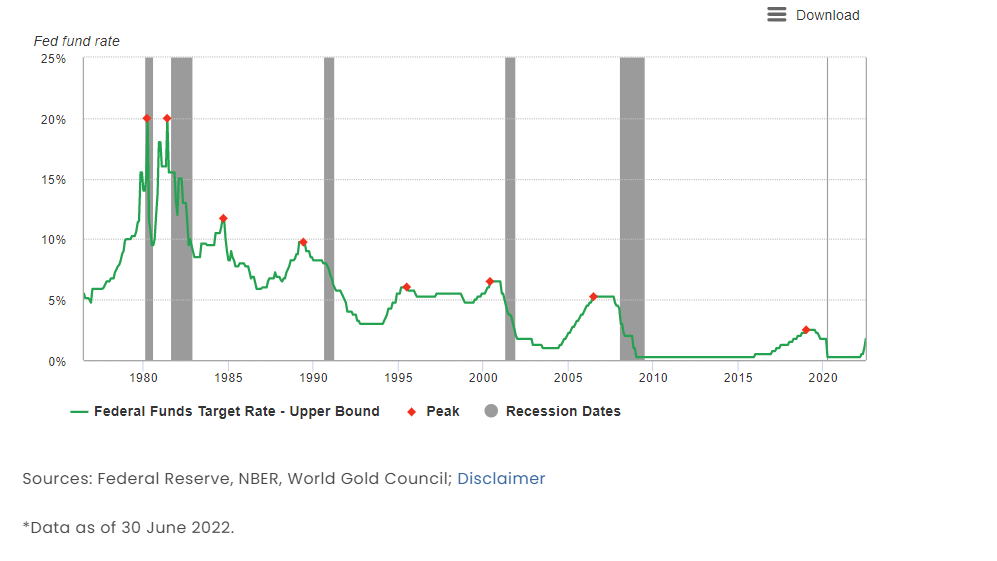

Identifying a target return to be achieved within a specific timeframe to cover all liabilities is important for DB schemes. But achieving that outcome with any level of certainty can be difficult. One of the most important questions for investors today is whether the higher interest rates that are arriving hard and fast can indeed bring about a “soft landing” for the global economy. Past experience suggests that this will be difficult; tightening has often preceded downturns.

Since 1976, for example, the Fed has only twice succeeded in hiking rates without subsequently pushing the US economy into a recession in the following couple of years – in 1983 and 1994 (Chart 3). Only time will tell whether the Fed’s latest hiking cycle will succeed in combating inflation without a recession – or if a recession will be needed to kill inflation.

Chart 3: Fed funds rate hikes have usually resulted in a US recession

Six out of the past eight hikes have followed this pattern*

What makes gold a strategic asset for DB pension funds?

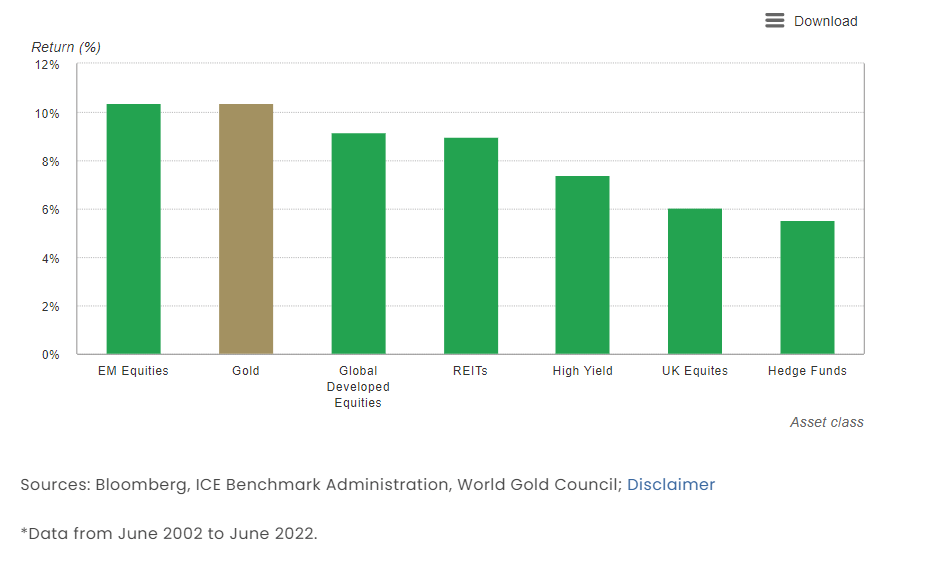

Our analysis shows gold is a clear complement to equities and broad-based growth portfolios. A store of wealth and a hedge against systemic risk, gold has historically improved portfolios’ risk-adjusted returns, delivered positive returns, and provided liquidity to meet liabilities in times of market stress.

Investors have long considered gold a beneficial asset during periods of uncertainty. Yet, historically, gold generated long-term positive returns in both good and bad economic times, outperforming many other major asset classes over the past 20 years (Chart 4).

Chart 4: Gold has outperformed most broad-based portfolio components over the past two decades

Annualised returns of key global growth-oriented assets in GBP*

The diverse sources of demand give gold a particular resilience and the potential to deliver solid returns in various market conditions. Gold is, on the one hand, often used as an investment to protect and enhance wealth over the long term, but on the other hand it is also a consumer good, via jewellery and technology demand.

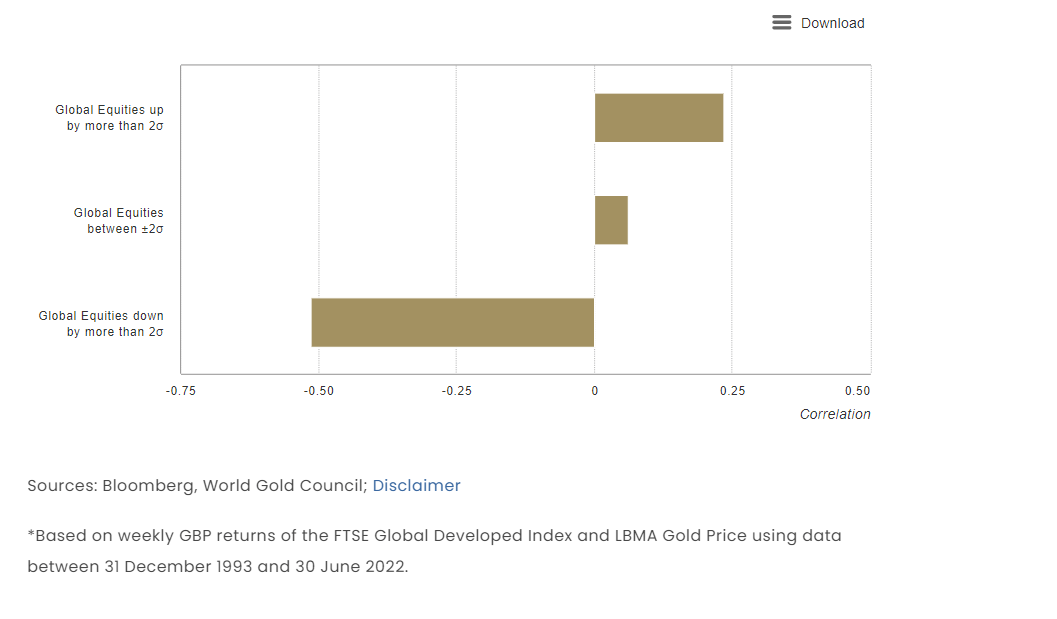

Furthermore, while effective diversifiers are sometimes hard to find, with many assets becoming increasingly correlated as market uncertainty rises, gold is different in that its negative correlation to equities and other risk assets increases as these assets sell off (Chart 5).

Chart 5: Gold becomes more negatively correlated with equities in extreme market selloffs

Correlation of global equities vs. gold in various market environments*

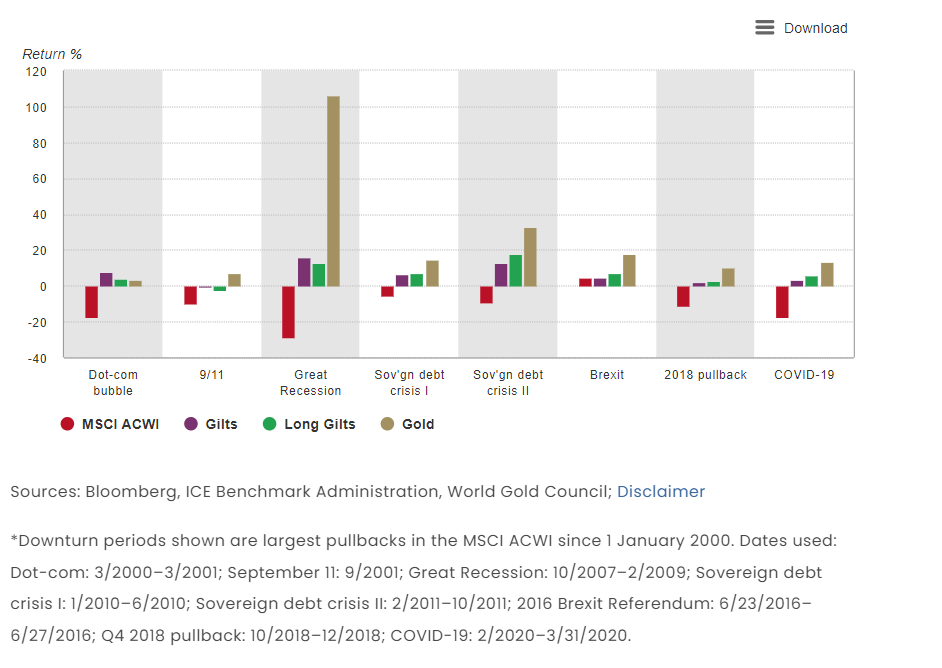

With few exceptions, gold has been particularly effective during times of systemic risk, delivering positive returns and reducing overall portfolio losses (Chart 6).

Chart 6: Gold provides downside protection

Global equities, UK Gilts and gold returns (in GBP) during periods of systemic risk*

A DB portfolio including gold can help reduce funding ratio uncertainty

Let us now illustrate how an allocation to gold in a DB portfolio could help reduce funding ratio uncertainty and increase the chances of achieving a pension scheme’s endgame.

Table 1 (p.4) outlines two hypothetical schemes. We assume each scheme has a target time horizon of 10 years to become fully funded and has the same initial funding level (85%). We also assume that the trustees of these schemes are comfortable employing a leveraged Liability-Driven Investment (LDI) strategy to stabilise their funding ratios and have a target hedge ratio equal to the initial funding ratio.

For modelling purposes, we also assume both schemes have a required return of 4.3% with an asset mix of 30% return-seeking / 35% credit / 35% liability-hedging and a level of leverage of 3 in the matching portfolio. The first scheme has a typical return-seeking asset allocation, i.e. global equities. The second scheme holds a diversified mix of equities and gold.

Table 1: Hypothetical schemes with the same time horizon but different growth portfolios

Key characteristics and strategic asset allocation of two hypothetical schemes*

Chart 7: The uncertainty of reaching the chosen endgame could be reduced with an allocation to gold

Paths taken by two hypothetical schemes to become fully funded*

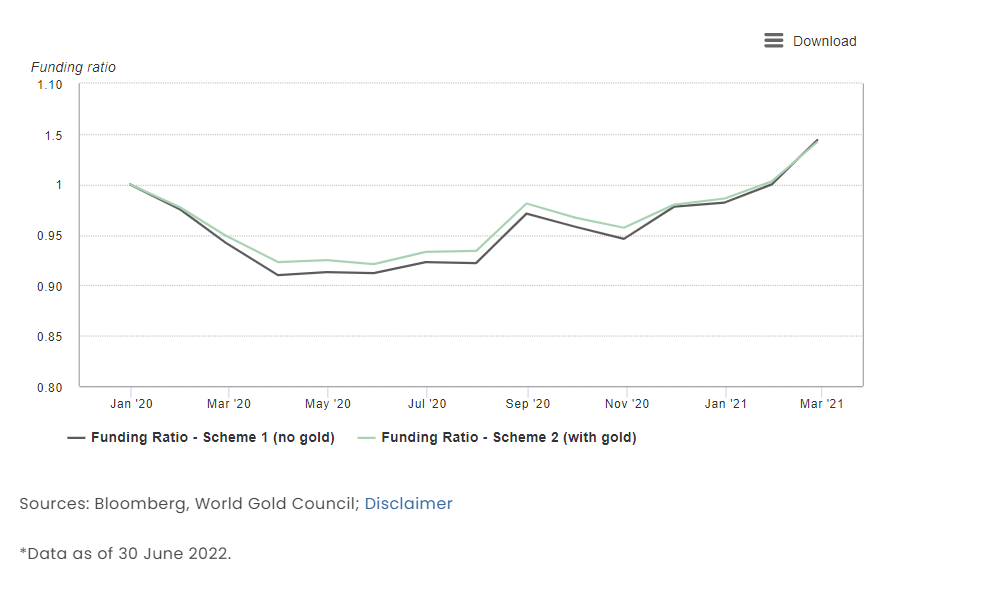

Moreover, funding level volatility can have a material impact on pension schemes. We witnessed this during the market turmoil of March 2020. Next, we compare how our two hypothetical schemes would have fared over that period – assuming no leverage for simplicity and an initial funding ratio of 100%.

The hypothetical scheme with a gold allocation did see a reduction in the funding ratio volatility, reaching a level of 0.93 vs. 0.91 for a scheme without gold (Chart 8). The benefits of this scheme’s shallower drawdown are twofold: assets are not required to work as hard to recover, and the management of a sponsoring employer’s balance-sheet risk is also helped.

Chart 8: An allocation to gold could have reduced the funding ratio volatility during the COVID-19-induced crisis

Funding ratio of two hypothetical schemes with and without gold*

Conclusion

Following significant funding level volatility over the last two years, there is a sharper focus on risk management among DB schemes. The potential higher returns from an equity exposure will continue to be important, particularly for schemes looking to reduce the time to their long-term funding target, close any funding gaps, and provide a buffer against longevity risk. Nevertheless, schemes focused on maximising outcome certainty should have a preference for an asset mix which provides a higher level of certainty of achieving those returns over a specified timeframe.

As demonstrated in our hypothetical case study, an allocation to gold can help mitigate the key risk faced by DB schemes – namely, uncertainty of being able to pay pension benefits – by providing long-term growth potential and diversification that helps reduce funding level volatility.

Appendix

Asset class forecasts:

- Equities & UK corporate bonds: we have used State Street Global Advisors’ Q3 long-term asset class forecasts. These forecasts are forward-looking estimates of total return, generated through a combined assessment of current valuation measures, economic growth, inflation prospects, ESG considerations, yield conditions, as well as historical price patterns

- The matching portfolio is modelled using the yield to maturity of 20-year nominal UK government bonds with cost of leverage modelled using SSGA Q3 2022 long-term asset class forecasts for UK cash

- Gold is modelled using Qaurum. The World Gold Council has developed a framework to better understand gold valuation. Our Gold Valuation Framework powers our web-based tool, Qaurum, which allows users to assess the potential performance of gold under customisable hypothetical macroeconomic scenarios. For the analysis, we have used an expected return of 3.5%, which is the average long-term implied gold return across the five pre-defined macroeconomic…

Read More:Investment Update: The Case For Gold In U.K. Defined Benefit Pension Schemes

2022-09-03 12:08:00