da-kuk/E+ via Getty Images

This article was first released to Systematic Income subscribers and free trials on Jan. 8.

Welcome to another installment of our Preferreds Market Weekly Review where we discuss preferreds and baby bond market activity from both the bottom-up, highlighting individual news and events, as well as top-down, providing an overview of the broader market. We also try to add some historical context as well as relevant themes that look to be driving markets or that investors ought to be mindful of. This update covers the period through the first week of January.

Be sure to check out our other weekly updates covering the BDC as well as the CEF markets for perspectives across the broader income space.

Market Overview

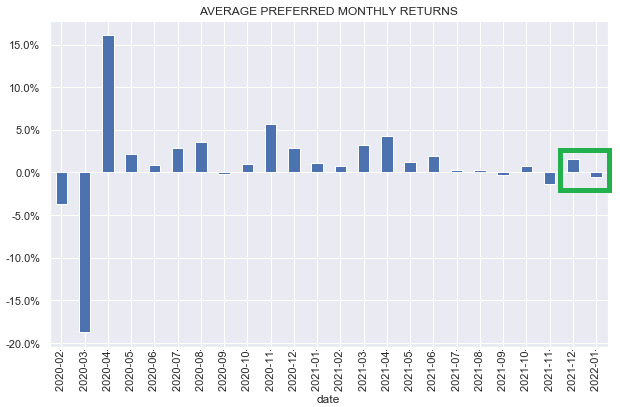

The preferreds market continues its “fat and flat” see-saw price action pattern. While the December Santa Rally delivered the strongest monthly return since June of last year, January has been disappointing so far.

Systematic Income

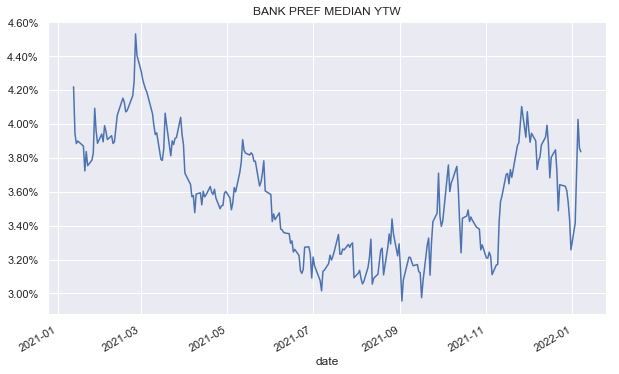

The biggest theme of the year so far has been the relentless rise in Treasury yields. Each trading day of the year brought higher longer-term yields and the 10Y yield now stands at 1.76% or 0.41% higher off its December low.

The knock-on effect of this rise in Treasury yields has been the rise in higher-quality preferred yields. The banks sector median yield-to-worst, for example, has risen closer to 4%. This makes taking low-coupon / duration exposure a bit more palatable in the current environment.

Systematic Income

The risk of higher rates is one that continues to hang over investors. However, higher rates is far from the only risk. A number of macro indicators are already suggesting we are moving into the mid-cycle period where the economy is more vulnerable to falling back into a recession. Longer-duration higher-quality preferreds provide an attractive allocation for this scenario as they can be supported by the typical pattern of lower rates in recessionary environments and their higher quality (i.e. investment-grade ratings) means they can weather a macro downturn.

A few securities worth highlighting in the space are the investment-grade and crossover rated preferreds such as the Capital One 4.375% Series L (COF.PL), JPM 4.2% Series MM at a 4.4% yield, (JPM.PM) at a 4.26% yield and Wells-Fargo 7.5% Series L (WFC.PL) at a 5.1% yield.

Market Themes

There was a quick exchange on Amtrust preferreds on the service chat this week. These preferreds were delisted by the issuer when the company was taken private with the comment that it was too burdensome to maintain the required regulatory reporting. The company also recently accepted a $10m civil penalty from the SEC relating to its loss reserve estimates. The preferreds are non-cumulative and yield around 10%.

Investors are basically worried that the company will suspend dividends and leave them in the lurch. Though this seems unlikely for a financial issuer, the preferreds are already trading around 25% below liquidation preference so the market clearly thinks the risk is not trivial. Admittedly, some of the drop is probably due to the SEC No Pink Info rule which can make it hard to trade them, causing many holders to dump the stocks.

To partly hedge against the risk of dividend suspension, it can pay for investors to limit holdings from issuers that are 1) private, 2) trade OTC / No Pink Info, 3) are non-cumulative and 4) issue infrequently if at all. The reputational / operational risk of stopping dividends is less of a concern for these issuers than for ones that don’t fit these criteria.

A good example here is the mREIT preferreds sector. The issuers in the sector are very unlikely to delist their preferreds because they are relatively frequent and sophisticated issuers so they require a consistent access to funding markets, particularly $25-par preferreds. They are also cumulative issuers which means they have to continue to accrue the dividend even when suspended which creates an incentive to either continue to pay or reinstate it quickly.

Market Commentary

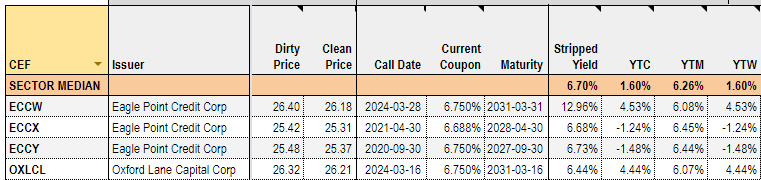

The CLO Equity CEF Oxford Lane Capital (OXLC) is issuing a new note. Relative to the Eagle Point Credit Co (ECC), OXLC has very little unsecured debt in its capital structure. And this is precisely what made something like OXLCL very attractive within the sector.

To provide some intuition here – the OXLC 6.75% 2031 Note (OXLCL) breakeven recovery rate is around 9% while the ECC note (ECCW, ECCX, ECCY) breakeven recovery rate is 20%. What this means is that OXLC assets can lose 91% of their value and OXLCL will still be whole while ECC assets can only lose 80% of their value before the notes will be impaired.

This better margin of safety for OXLC notes will worsen a bit with the breakeven recovery rising to 15% so OXLC notes will still have a more attractive credit profile versus ECC.

This is how the population of CLO Equity notes looks like at the moment. There are two notes that currently callable (ECCX, ECCY) and two that are callable in the future (ECCW, OXLCL).

Systematic Income Baby Bond Tool

The new OXLC note (OXLCZ) will have a 5% coupon and a January 2027 maturity. The other 2 not currently callable CLO Equity notes (ECCW) and (OXLCL) (both 2031 maturity) are trading at 4.44% and 4.53% YTW respectively. In this context, OXLCZ will look much more attractive, offering not only a higher yield of 5% (at “par”) but also a significantly shorter maturity.

There are also two ECC pinned-to-par notes with 2028 and 2027 maturities (ECCX, ECCY) that are trading at negative YTW (i.e. a small loss if redeemed immediately) but can occasionally be scooped up closer to a flat YTW and YTMs of 6.5% and which can also offer attractive holds.

Public Storage is out with a new investment-grade preferred (PASDV) at a 4.1% coupon, trading at a 4.15% yield. PASDV is currently trading at the highest yield in the suite with most PSA preferreds boasting yields well below 4%.

Overall, an investment-grade security at 4.1% is not too bad. Its low coupon does mean its duration will be on the high side (the smaller the coupon the more the price has to drop in order for the yield to rise a fixed amount to match a rise in Treasury yields). In an earlier article, we had a look at how stocks with different coupons behave during shifts in Treasury yields. In short, lower coupon preferreds will tend to be more volatile as their prices have to change more in order to generate the same change in yield.

In terms of our stance in the sector, we continue to execute on our lower-beta paybook with a focus on shorter-maturity, pinned-to-par and niche-sector securities. The recent shift in yields means we have a more favorable view on taking duration risk, however, we would first wait for Treasury yields to consolidate before adding duration exposure.

Read More:Preferreds Market Weekly Review: OTC Dividend Suspension

2022-01-16 09:29:00