Automakers need to do some serious navel-gazing about price levels and going upscale, if they want to sell more vehicles.

By Wolf Richter for WOLF STREET.

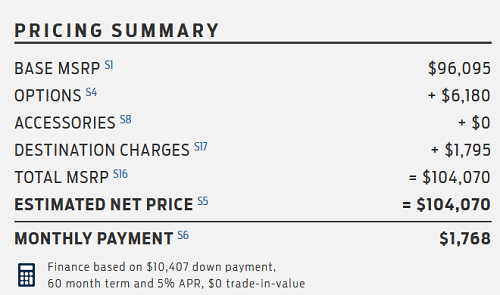

To illustrate the data we’re going to look at in a moment, I “built” a 2023 model year F-250 Lariat on Ford’s website: MSRP $104,070. I could build something more expensive in the F-350 lineup. Ford suggested to finance it with Ford Credit. With a down payment of $10,407, and a term of five years, at 5% APR, I would end up with a monthly payment of $1,768. Screenshot from Ford’s website:

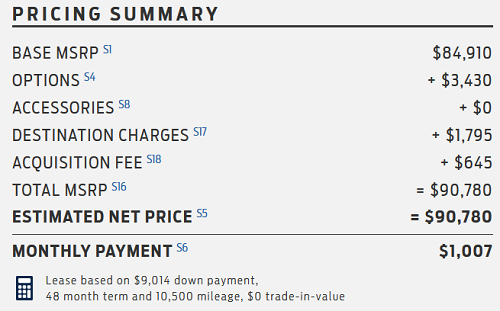

There is a wide range of options and trim packages, particularly among trucks. I also “built” a 2023 F-150 Lariat, and it ended up with an MSRP of $90,780. Ford suggested to lease it from Ford Credit with $9,014 down, over 48 months, for $1,007 per month. Screenshot from Ford’s website:

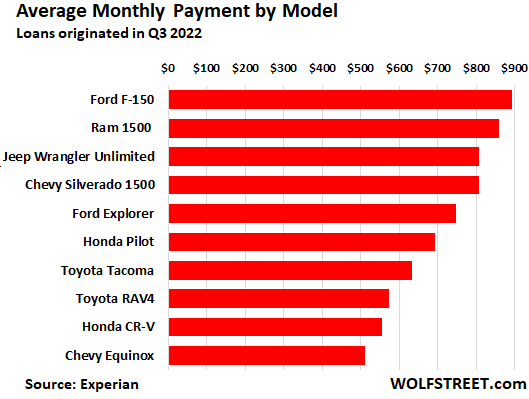

According to Experian’s State of the Automotive Finance Market report for loans originated in Q3 2022, the average monthly payment for the F-150 in Q3 rose to $893 a month; for the Ram 1500, it rose to $860; for the Chevy Silverado 1500, it rose to $808.

Pickup trucks have long been among the bestselling new-vehicle segments in the US. They’re a huge part of the business. Ford didn’t take EVs seriously until Tesla threatened to build a pickup five years ago. That’s when Ford got religion and dove into EVs and has come out with an electric pickup to defend its core turf, while we’re still listening to Tesla threatening to come out with one. Ford lives and dies by its pickups.

And automakers have taken them upscale over the past two decades because upscale is where the money is, and they’ve come out with high-end models and equipment packages that push pickups into the luxury segment, and they have jacked up prices, and they’re making huge profit margins on them.

But other popular vehicles have big payments too. These are the average payments for some models, according to Experian:

For all new vehicles, the average amount financed in Q3 – after down payments, trade-ins with spiking trade-in values, etc. – rose by 10.4% from a year ago to $41,665, according to Experian, up by 20% from Q3 2020 ($34,678).

The average new vehicle loan rate rose to 5.2% in Q3, up from 4.1% in Q3 2021 and from 4.2% in Q3 2020.

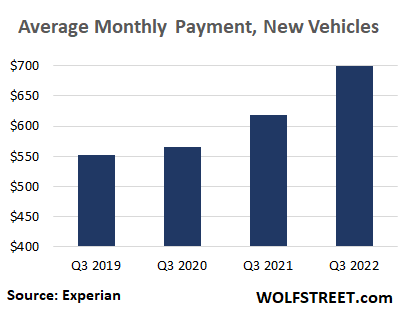

So the average new-vehicle loan payment jumped by 13% year-over-year to $700 a month. Over the past two years, the average payment spiked by 24% (from $565 in Q3 2020).

The average loan terms for new vehicles ticked up just a tad from a year ago, after dipping in the prior year:

- Q3 2019: 69.0 months

- Q3 2020: 69.6 months

- Q3 2021: 69.5 months

- Q3 2022: 69.7 months.

But there are differences: Buyers with a credit rating of “super prime” averaged the shortest loan term, while “near prime” and “subprime” averaged the longest terms:

- Super prime: 64.1 months

- Prime: 71.2 months

- Near Prime: 74.7 months

- Subprime: 74.2 months.

The share of loans with ultra-long loan terms grew; and interestingly, the share of short loan terms grew as well perhaps as buyers were trying to benefit from the lower interest rates in that range. But the share of the middle range, loans with terms of 5-7 years, declined:

- Up: 85 months and longer: share grew to 1.8% of total loan originations in Q3 2022, up from a share of 1.3% in Q3 2020.

- Up: 73-84 months: share grew to 34.6%, up from 28.9% in Q3 2020.

- Down: 61-72 months: share declined to 36.7%, from 44.6% in Q3 2020.

- Down: 49-60 months: back when I was in the business, this was as long as you could go; share declined to 16.6% from 19.7% in Q3 2020.

- Up: 48 months and shorter: interestingly, the share jumped to 10.3% from 5.5% in 2020.

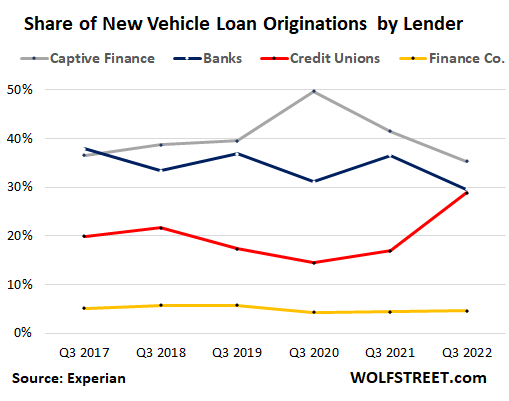

Who did the lending?

The share of credit unions jumped to 28.8% of all new vehicle loans originated in Q3 2022 (red line), while the share of banks declined to 29.5% (blue), and of the share automaker’s own finance divisions (“captive finance”), while still #1, dropped for the second quarter in a row, to 35.3% (gray):

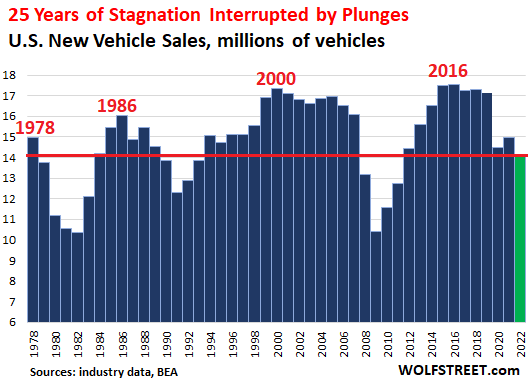

Dismal sales.

The sky-high costs of new vehicles – and the sky-high payments that they entail even at still relatively low interest rates – explain why, over the years, new vehicle sales volume in units has been a dismal affair for over two decades: sales in 2022 are on track to be where sales had been in the late 1970s.

This year was hobbled by supply chain entanglements. But even the Good-Times-2019 sales were below the sales in the year 2000.

If the auto industry wants to sell more vehicles, it needs to do some serious navel-gazing about price levels and going upscale (2022 includes the official WOLF STREET estimate for December sales, better than last December):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Read More:$1,768 a Month, with $10,407 Down, 5% APR, on a Ford Pickup? Update on Q3 New-Vehicle Finance

2022-12-06 01:30:00