What the Fed did in details and charts.

By Wolf Richter for WOLF STREET.

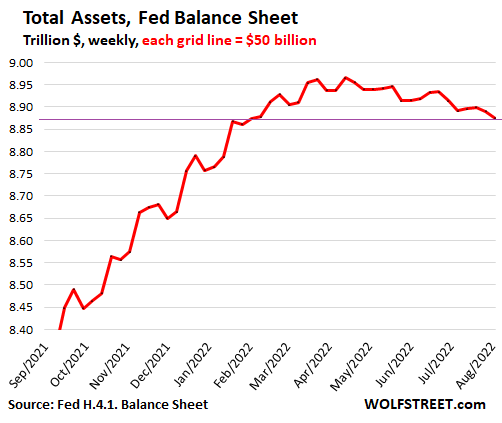

The Federal Reserve’s quantitative tightening (QT) finished its second month of the three-month phase-in period. Total assets on the Fed’s weekly balance sheet as of August 3, released this afternoon, fell by $17 billion from the prior week, and by $91 billion from the peak in April, to $8.87 trillion, the lowest since February 2.

QE created money that the Fed pumped into the financial markets via its primary dealers, from where it began circulating and chasing assets, including in non-financial markets such as housing and commercial real estate. The purpose and effect were to repress yields and create asset price inflation. And it finally also helped create raging consumer price inflation.

QT does the opposite: It destroys money and has all the opposite effects – not for day-traders but over the longer term. QT is one of the tools the Fed is using to crack down on this now raging consumer price inflation.

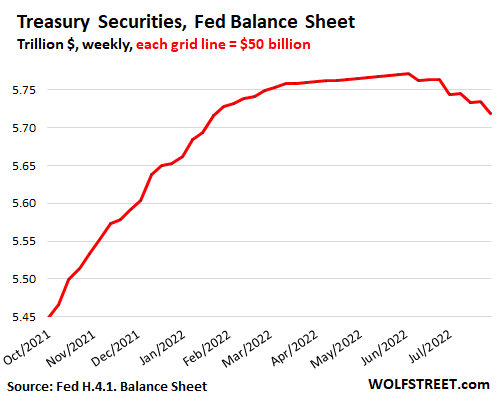

Treasury securities: -$52 billion from peak.

July: -$30 billion roll-off +$4.6 billion in TIPS Inflation Compensation.

Treasury notes and bonds roll off mid-month and at the end of the month, when they mature. Today’s balance sheet includes the roll-off at the end of July.

Treasury Inflation-Protected Securities (TIPS) pay inflation compensation that is added to the principal value of the TIPS. When TIPS mature, holders receive the amount of original face value plus the accumulated inflation compensation that was added to the principal.

The Fed currently hold $374 billion in TIPS. The amount of inflation compensation amounts to about $1 billion to $1.5 billion per balance-sheet week, or about $4 billion to $5 billion per calendar month, which adds to the balance of Treasury securities.

The QT phase-in plan (from June through August) calls for the Fed to let $30 billion in Treasury securities roll off per calendar month, as they mature. And the Fed did exactly that in July.

So why did Treasury securities decline by only $25.2 billion, and not $30 billion that rolled off? TIPS inflation compensation!

- The Fed let $30 billion in Treasuries roll off without replacement, which reduced the balance by $30 billion.

- The Fed received from the government $4.6 billion in inflation compensation, which increased the balance by $4.6 billion

- Net effect: the total balance fell by $25.2 billion.

Inflation compensation being added to the balance of Treasury securities every week is why the reduction in the balance will be less every month than the actual roll-off.

In the chart below, note the steady increase of around $1-1.5 billion a week after QE had ended from mid-March through June 6, which is the inflation compensation from TIPS.

The amount of Treasury securities has now fallen by $52 billion from the peak on June 6, to $5.72 trillion, the lowest since January 26:

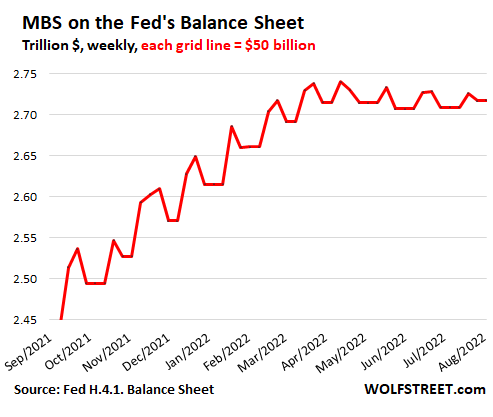

MBS, the peculiar creatures with the big delay.

How MBS can come off the balance sheet:

- Pass-through principal payments – the primary way

- When issuers “call” MBS

- When MBS mature, but they’re usually “called” before they mature

- When the Fed sells them, which it has said it might do some day in the future.

Pass-through principal payments: When the underlying mortgages get paid off (due to a sale or refi of the property) or when regular mortgage payments are made, the mortgage servicer (the company you send the mortgage payments to) forwards the principal payments to the entity that securitized the mortgages into MBS (such as Fannie Mae), which then forwards those principal payments to the holders of the MBS (such as the Fed).

The book value of the MBS shrinks with each pass-through principal payment. This reduces the amount of MBS on the Fed’s balance sheet. These pass-through principal payments are uneven and unpredictable.

The issuer “calls” the MBS. After a good number of years of pass-through principal payments, the remaining book value of the MBS may have declined so much that its not worth servicing the MBS any longer, and the issuer, such as Fannie Mae, decides to “call” the MBS to repackage the remaining mortgage debt into new MBS together with other mortgages. When Fannie Mae “calls” the MBS, they come off the Fed’s balance sheet.

When MBS mature. MBS have 15-year or 30-year maturities. But this is largely irrelevant because the average lifespan of mortgages in the US is less than 10 years because they get paid off due to a sale or a refi. And when the remaining book value of the MBS falls below a certain level, the issuer calls them, and gets them off the books.

How MBS get on the balance sheet.

The Fed purchased MBS in the “To Be Announced” (TBA) market during QE, and to a lesser extent during the Taper, and to a minuscule extent in June and July. The June and July purchases are designed to replace pass-through principal payments of June and July that exceeded the monthly cap of $17.5 billion.

But purchases in the TBA market take one to three months to settle. The Fed books its trades after they settle.

So the influx of MBS onto the balance sheet over the past few weeks are from trades that were executed a few months ago, before QT. What we’re now seeing are the purchases made during the Taper.

These purchases are not aligned with the pass-through principal payments that the Fed receives. This misalignment, and the three-month lag, creates the ups and downs of the MBS balance, that is then also visible in the overall balance sheet.

MBS: -$23 billion from peak to $2.72 trillion:

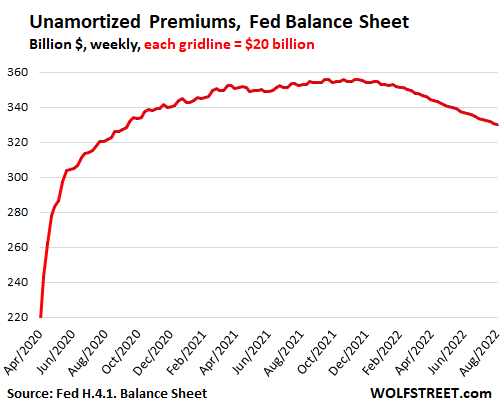

Unamortized Premiums: steady decline.

All buyers pay a “premium” to buy bonds if the coupon interest rate of that bond exceeds the market yield at the time of purchase.

The Fed books securities at face value in the regular accounts and it books the “premiums” in a special account, “unamortized premiums.” The Fed then amortizes the premium to zero over the remaining maturity of the bond, while it receives over the same time the higher coupon interest payments. By the time the bond matures, the premium has been fully amortized, and the Fed receives face value, and the bond comes off the balance sheet.

The “unamortized premiums” peaked with the beginning of the taper in November 2021 at $356 billion and have now declined in a steady process by $26 billion to $330 billion:

The other QE and bailout assets are largely gone.

- Special Purpose Vehicles (SPVs) through which the Fed bought bonds, loans, and ETFs: $38 billion

- Central bank liquidity swaps: $0.2 billion.

- Repos: $0

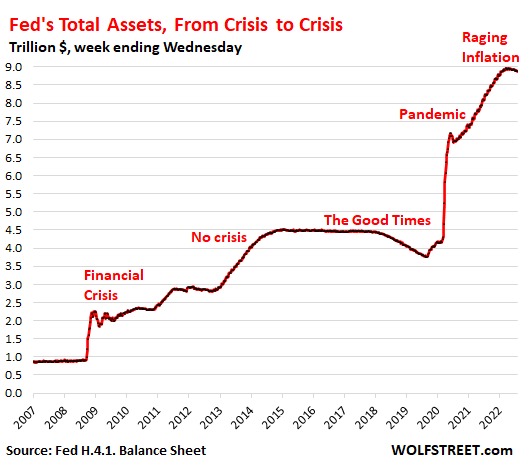

Money-printing comes home to roost:

In the 15 years of this chart, there are three crises: The Financial Crisis, the Pandemic, and now Raging Inflation. Today’s inflation crisis pulls into the opposite direction of the prior two crises, and dealing with it will require the application of the tools in the opposite direction:

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Read More:Fed’s QT: Total Assets Drop by $91 Billion from Peak (QE created money, QT Destroys Money)

2022-08-05 06:06:03