“The rate of decline is far worse than what we saw through the previous downturn. Affordability is more stretched, household indebtedness is higher and then this dual factor of inflation and rising interest rates is more hard hitting,” says Tim Lawless, Asia-Pacific research director at CoreLogic.

This means the biggest factor at play in determining when house prices will start to rise again is interest rates, and when the RBA will begin a cycle of cutting them once again.

“When we see start to see interest rates levelling, which will probably be somewhere around the middle of next year, if not earlier than that, that’s probably the cue that housing markets will start to stabilise,” says Mr Lawless.

Two signs that we might be approaching the peak of the rate cycle is that inflation starts to head back down towards its target range of 2-3 per cent, and that the tight labour market begins to loosen.

Do downturns (and upswings) follow certain patterns?

Yes, there are certain characteristics that property cycles in Australia tend to have in common.

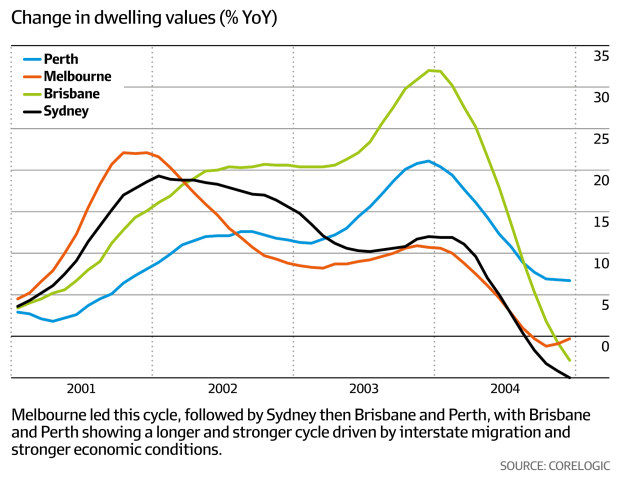

First, when it comes to the capital cities, you tend to see Sydney and Melbourne lead the cycle and smaller cities such as Brisbane and Adelaide follow. Although there are exceptions.

“Perth, for example, is quite disconnected and much more driven by the commodity cycle and major infrastructure projects, and the same with Darwin. And then there are the regional markets that are more agricultural, for example, and are more divorced from the broader trends,” Mr Lawless adds.

Domain’s chief of research and economics, Nicola Powell, says Sydney and Melbourne tend to record greater price swings compared to other capital cities because homeowners are more sensitive to changes in economic conditions.

“Generally speaking it’s where incomes are higher, households are more indebted and there’s greater investment activity proportionately … so you tend to see bigger swings, both in price gains in an upswing, but they are also more vulnerable in a downturn,” Dr Powell says.

What if you drill down to a city level?

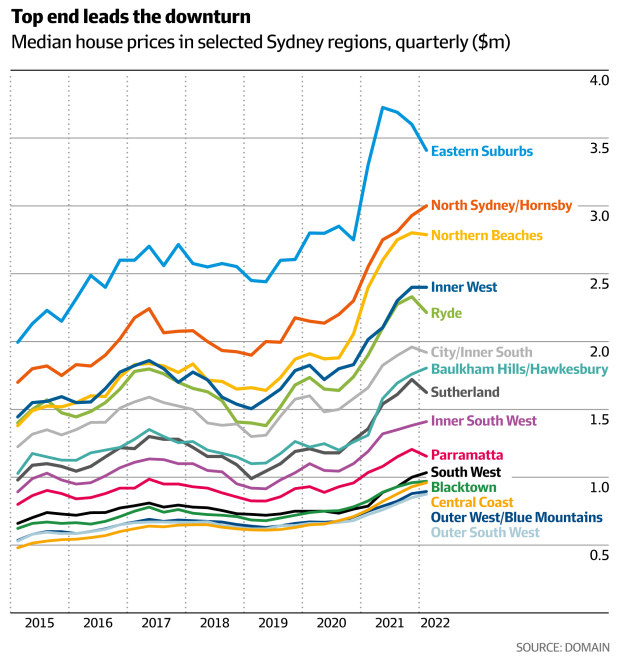

In the same vein, higher-priced suburbs and regions within a city are often the first to show signs of a downturn, or an upswing, before it spreads elsewhere.

Sydney’s eastern suburbs reached a house price peak back in June 2021, so the eastern suburbs have already registered three consecutive quarters of house price declines.

At the lower end of the market, in regions like Blacktown, Central Coast and south-west Sydney, house prices are still rising.

So if you are trying to pick the bottom out the cycle, keep a close eye on the higher-priced areas, says Dr Powell.

“When we move into a recovery phase we are likely to pick that up first in the upper end, and the eastern suburbs is one of those areas,” she adds.

How long do property downturns usually last?

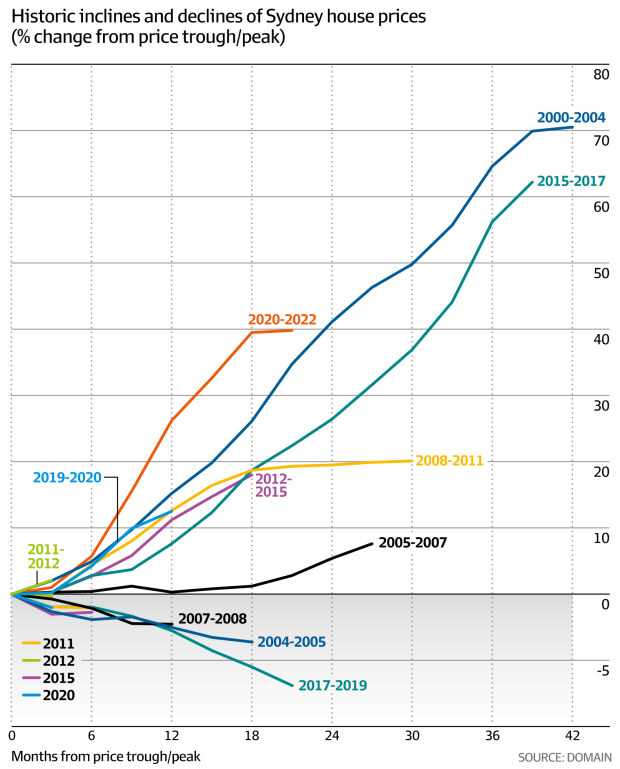

A recent analysis by Domain that observed the duration of market cycles in Sydney, found that the downturns tended to last less than half the amount of time (in months) than the preceding upswing.

“The downturns are shorter and less severe than what was seen in the upswing, generally speaking,” says Dr Powell.

For example, the property boom between 2000 and 2004 lasted 42 months until reaching its peak, whereas during the downturn that followed, it took just 18 months for prices to fall from the peak to the next trough.

Mr Lawless points out that through every down phase, the annual gain in housing values in the 12 months leading up to the market peak has been equal to or higher than the entire peak to trough decline that follows.

“Over a two-year period ahead of each market peak, capital gains were always more substantial than the subsequent peak to trough decline,” he adds.

Is it possible to pick the bottom of the market?

Mr Lawless says people should time their decision to buy a property on their own circumstances and budgets.

“The reality is, trying to pick the top and bottom of the market is impossible,” he says.

Nevertheless, there are several key indicators – a combination of macroeconomic and housing market factors – that the market may be on the cusp of a turnaround.

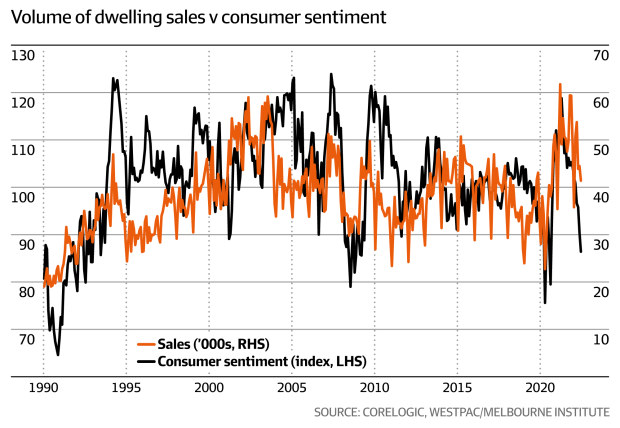

How consumer sentiment is tracking (as recorded in a weekly ANZ-Roy Morgan survey and a monthly Westpac-Melbourne Institute survey) offers a timely and “close to perfect” correlation with the housing market.

Any improvement in consumer mindsets (a person’s willingness to buy a major household item, or their outlook around family finances for the 12 months ahead) will give you an indication that things are also starting to looking up for the property market.

“The correlation is not perfect, but it’s close to perfect,” says Mr Lawless.

“It really highlights that as consumers feel more pessimistic about their own balance sheets, about interest rates, about their prospects for employment, that has a negative flow on effect to housing demand.”

Property indicators include the number of listings, the average selling time of properties as well as discounting rate from vendors.

The number of people attending, as well as the number of bidders, at auction, as well as auction clearance rates (the percentage of properties that sold at auction on a particular weekend) offer a good barometer of the market, adds Dr Powell.

“Sixty per cent is considered the benchmark for clearance rates, so if they fall below that it normally shows the market is correcting, and we are going to see prices fall – and obviously the reverse, for when you get above 60 per cent.”

Sydney’s auction clearance rate last week fell to 49.9 per cent, the first time it has dropped below the 50 per cent mark since mid-April in 2020.

Is it better to sell or buy first in a downturn?

There’s no one-size-fits-all answer for this, but because the top end of the market tends to lead the downturn, it may create a “sweet spot in timing” for a particular buyer segment – the upgrader – says Dr Powell.

If you’re buying into a market where prices are falling first, ideally you would sell your (smaller, less valuable) home while prices are still firm, and then buy into the higher-end market once prices have continued to fall.

Of course, that scenario doesn’t consider how hard it might be to find a new house, and once you’ve sold, you could be left in the lurch.

Read More:How to tell when house prices will hit bottom

2022-07-08 00:15:00