ferrantraite/E+ via Getty Images

Co-produced by Austin Rogers

Your Personal Home: Investment Or Expense?

We hear it repeated all the time: Buying a personal home is a great long-term investment. Most of the time, this statement is given without any supporting argument but rather simply assumed to be the case.

“Of course, homeownership is a good investment,” people think. “It has to be better than just throwing money away by renting because I’m building equity in a real asset.”

But there are two counterpoints to be made in response:

- Homeownership is not necessarily a better financial decision than renting.

- One’s personal home, whether owned or rented, should be considered an expense, not an investment.

These points are important to understand because one of the most commonly cited reasons we hear from investors who avoid real estate investment trusts (“REITs”) is that they already have a large portion of their net worth invested in real estate via their personal residence.

We believe this is a mistake for the two reasons cited above. Let’s discuss these reasons in more depth and finish by highlighting the benefits of an allocation to REITs whether one owns a home or rents.

Renting Vs. Owning

Many people assume that buying a home is always the better financial decision than renting one, but that is not necessarily the case.

While many would point to the drop in mortgage rates the last few years, consider also the differential in home price growth versus rent growth.

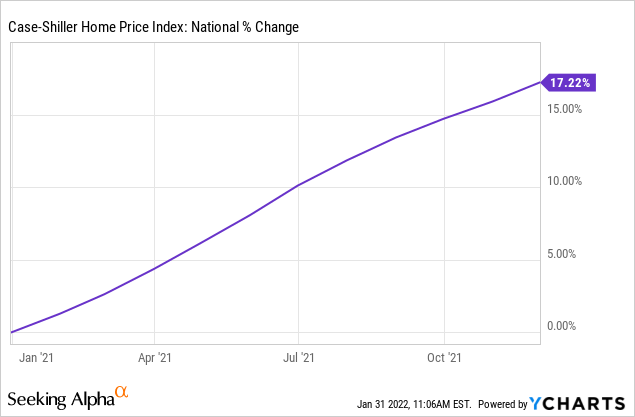

In 2021, according to the Case-Shiller Home Price Index, the nationwide average home price surged over 17%.

Home price appreciation (YCHARTS)

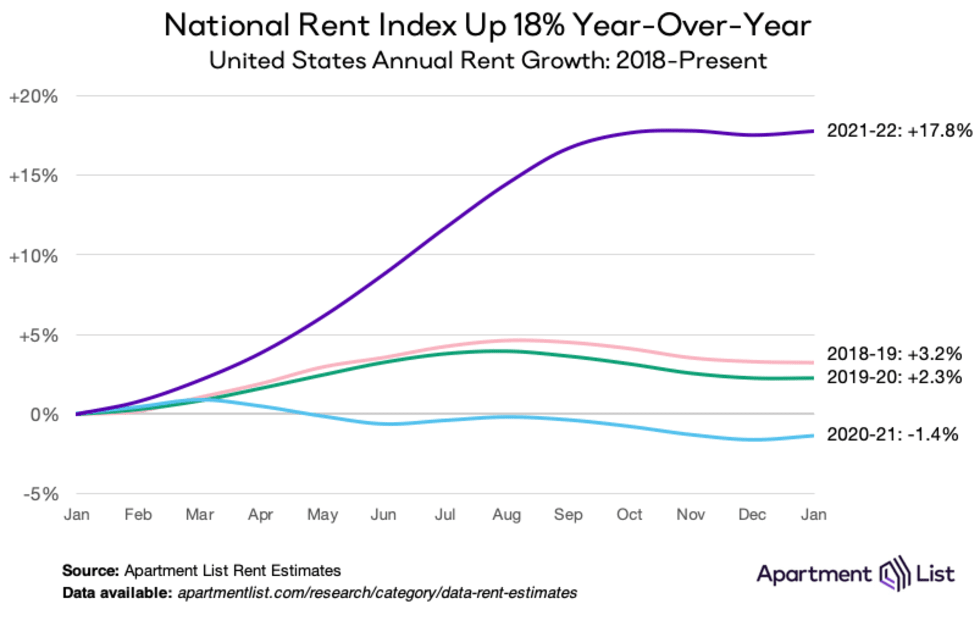

Admittedly, according to Apartment List, the nationwide average rent rate rose a touch higher – 17.8%.

National rent growth (Apartment List )

But there is a crucial point to keep in mind when comparing roughly equal rent and home price growth from 2021, and that is the year they followed. In 2020, home prices rose over 10%, while the nationwide average multifamily rent rate declined by 1.4%.

So, in the two full years from the beginning of 2020 to the end of 2021, home prices rose over 25% while multifamily rents rose only about 16.5%.

To determine whether it is a better financial decision to rent or buy, one must calculate the total costs of renting versus buying.

For renting, total costs include rent, facility fees, any non-refundable deposits, pet rent, utilities, Internet, and any other recurring fees.

For owning, total costs include principal and interest payments (aka, the monthly mortgage payment), home insurance, real estate taxes, utilities, Internet, regular maintenance such as lawn care and pest control, as-needed repairs, and also the opportunity cost of having all that principal tied up in the property.

When calculating the cost difference between renting and buying, people often forget to amortize the expected costs of replacement for major household items, such as:

- Roof

- Appliances

- Water heater

- Air conditioner

- Fencing (if applicable)

- Garage door (if applicable)

The expense of replacing any one of these can reach thousands of dollars and single-handedly make buying more expensive than renting. Remember that when renting, the landlord is responsible for these major repairs/replacements, not the tenant.

Another often-overlooked point on this subject is that people tend to spend more money sprucing up their home if it is an owned property rather than a rented one. This is natural, of course, and people are often happy to spend more money on landscaping and interior design for a home they own than one they rent. But it needs to be factored into the rent vs. buy cost comparison.

In May 2021, LendingTree released a study showing that, when comparing only monthly payments, it is cheaper to rent than to own a home with a mortgage in all of the nation’s 50 largest markets. On average, it is $606 cheaper to rent than to own across these top 50 markets.

The study found that renting is especially cheaper than buying in expensive coastal markets like New York City and San Francisco, but it is also cheaper in less expensive cities like Orlando, Tampa, and Indianapolis.

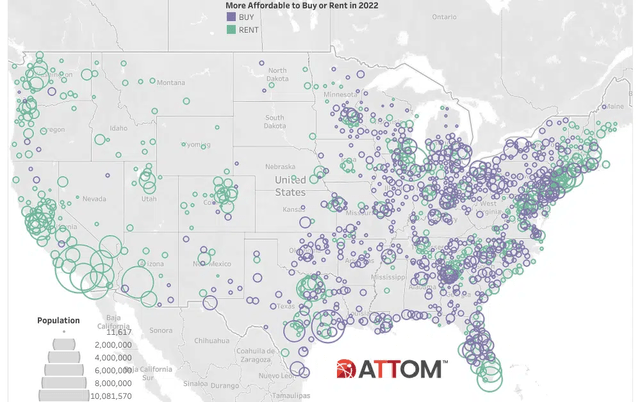

Using more recent data and a different methodology, the 2022 Rental Affordability Report put out by ATTOM Data Solutions is more favorable to buying than renting, but even this report shows that it is cheaper to rent than buy in 35 of the 42 US counties with a million or more residents.

Housing affordability: Buy vs. Rent (ATTOM Data Solutions)

Moreover, in 1,015 of the 1,154 counties ATTOM analyzed for the report, the median price for a three-bedroom home was rising faster than the median rent for a three-bedroom home. If this situation persists, it will become increasingly cheaper to rent than buy even using ATTOM’s methodology.

Unsurprisingly, ATTOM attests that it remains more affordable to own than rent in less densely populated counties. But both the LendingTree and ATTOM studies use only recurring monthly costs for the comparison while ignoring the inevitable costs of homeownership relating to occasional repairs and “lifestyle inflation.”

What’s more, comparing apples to apples (a 3-bedroom home for sale and a 3-bedroom rental home) when it comes to renting vs. buying may seem reasonable, but most people increase their home size and quality when they go from renting to owning. As such, their total housing costs tend to rise as well.

Housing Is Not An Investment

The word “investment” tends to be used quite liberally, referring to a great many things. But in the most literal sense, an investment is the allocation of money to some use that is intended to generate a return on that invested money.

With this in mind, then, it makes little sense to think of one’s home as an investment. The primary purpose of one’s home is not to generate a return but rather to provide for an essential need – that is, to put a roof over one’s head. This is true whether one is renting or owning.

Now, one would naturally object here that homeownership builds equity in a real asset, while renting does not. But what if the total, all-in cost of renting is less than it is for owning? And what if one invests the difference in cost between renting and owning in the stock market or REITs?

Assuming the all-in cost of renting is lower than owning, investing the money that one saves by renting into other assets is an alternative way of building equity.

As we saw in the previous section, it is cheaper to rent than buy in the country’s most populated areas. But even in cases where it is cheaper to own than rent, personal homeownership still isn’t an investment. This is not only because a home is meant to provide for an essential need, but also because it often does not generate a positive return on investment if one considers all money spent on the property.

If one includes the costs of repairs, maintenance, replacements, renovations, upgrades, and other non-recurring costs, then one’s total money spent on the home frequently doesn’t result in much of a return, if any, when one sells the property.

An Actual Real Estate Investment

The point of the preceding sections is not that it is always a better financial decision to rent than to buy. That is a decision each person must make on their own, depending on one’s unique situation.

Rather, the point is that whether one rents or owns, one’s personal residence is an expense, not an investment. As such, it makes no sense for homeowners to avoid real estate investments simply because they own a home. It is a fundamentally different concept to own real estate for one’s personal use and to own it for investment purposes.

Given the income-generating and inflation hedging properties of real estate, it is not a good idea to avoid it because one owns their own home. After all, one derives no rental income from their personal residence, and this negates much of the inflation protection that investment real estate provides.

Publicly traded REITs (VNQ) have historically been a great way to generate income, providing over double the dividend yield of the S&P 500 (SPY). But they have also provided very respectable total returns over time as well.

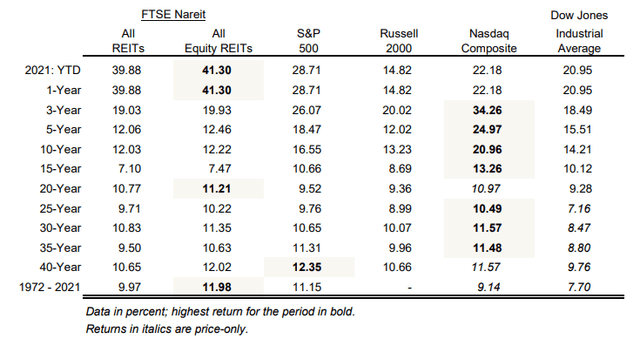

Last year, equity REITs enjoyed a very nice run, but they also outperformed SPY and the Nasdaq Composite’s (QQQ) tech stocks over the last 20 years.

REIT performance vs. other asset classes (NAREIT)

Moreover, as you can see above, REITs outperformed all other publicly traded stock types over the 49-year period from 1972 to 2021, providing a roughly 12% annualized return.

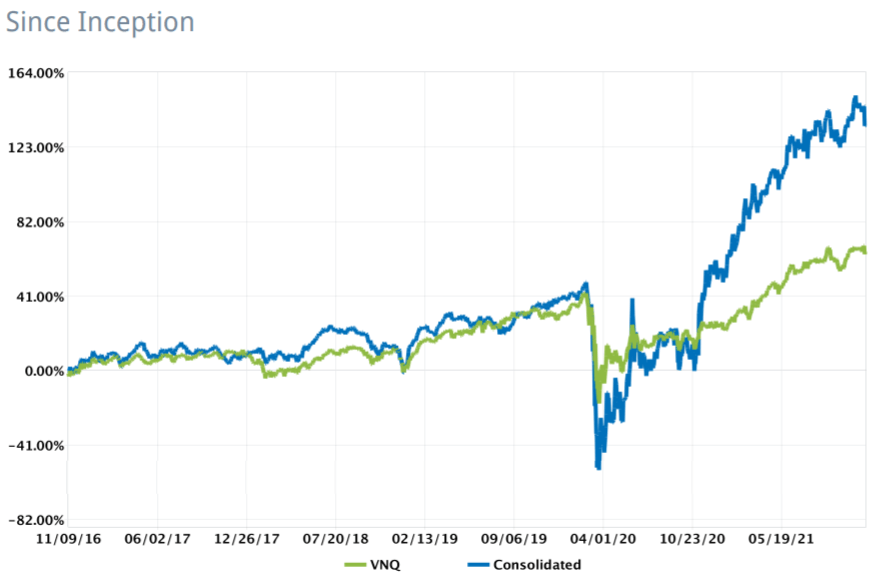

However, for those wanting to invest in real estate, it is possible to outperform both the broader REIT index as well as the stock market by concentrating only on the strongest compounders and most attractive upside plays. That is exactly what we do at High Yield Landlord, and this strategy has served us well since we founded our portfolios:

High Yield Landlord vs. VNQ (Interactive Brokers)

Today, our REIT Portfolio includes 24 cherry-picked companies from a universe of over 200 investment options.

To give you a few examples:

We invest heavily in Medical Properties Trust (MPW), which is the largest hospital REIT in the world. It pays a 5% dividend yield and it is able to grow its cash flow by 6-8% per year by hiking rents and acquiring new properties. Historically, it has been a strong outperformer and we expect the market-beating returns to continue for years to come.

Hospital owned by MPW (Medical Properties Trust)

We also invest in VICI Properties (VICI), which is the owner of trophy casino properties like the Caesars Palace (CZR) in Las Vegas. Its leases are 40+ year long on average, include automatic rent increases, and all property expenses including the maintenance are the responsibility of the tenant. Just like MPW, VICI has a simple formula that should deliver double-digit total returns in the long run, combining a 5% dividend yield and 6-8% annual growth.

Trophy casino owned by VICI (VICI Properties)

We like to target…

Read More:REITs: Your Personal Home Is Not A Real Estate Investment

2022-02-05 14:00:00