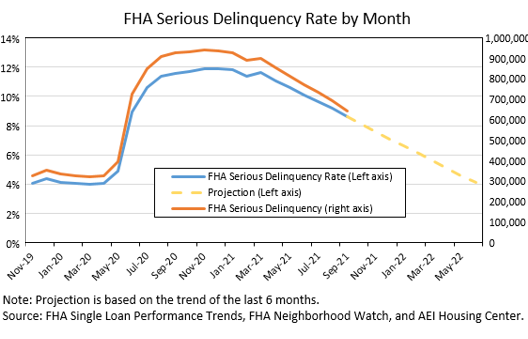

8.5% of FHA mortgages are still seriously delinquent — accounting for half of all seriously delinquent mortgages.

By Wolf Richter for WOLF STREET.

The FHA – a government agency that insures 7.5 million high-risk, low-down-payment mortgages, including subprime mortgages – has been at the core of the pile-up of delinquent mortgages during the period of the foreclosure moratorium and forbearance, when borrowers didn’t have to make mortgage payments.

Among FHA-insured mortgages, serious delinquencies (90+ days behind) have been dropping since the 12% peak in February. By the end of September, 8.5% of FHA mortgages, or 632,000 mortgages, were seriously delinquent, according to a report by the AEI Housing Center. This is still far higher than the rate before the pandemic of just over 4%, and accounted for over half of all seriously delinquent mortgages, though FHA mortgages account for only 17% of all mortgages.

The foreclosure moratorium ended on July 31. When the forbearance period ends for each mortgage depends on the borrower and when the mortgage was entered into a forbearance agreement. For more and more of these mortgages, forbearance is terminating, and this is when the borrower needs to deal with reality, of sorts.

How can a borrower exit the forbearance agreement?

Given the surge in home prices, many borrowers can sell the home for more than the balance of the mortgage; and they would then pay off the mortgage in full, thereby fix the arrearage, cover the selling expenses, and may even have some cash left over. This might be a great time to sell a home, after that kind of run-up in prices. And it solves the problem.

If borrowers can resume making normal payments on the existing mortgage, the missed payments will be added to the end of the mortgage, which moves the mortgage into “current” status.

If borrowers cannot resume making normal payments, they can work out a deal to have the mortgage modified to stretch out the term of the mortgage and lower the payments. If that doesn’t work, they can sell the home and pay off the mortgage.

Borrowers face foreclosure if they cannot meet the requirements of even a modified mortgage, and cannot sell the home for enough to pay off the mortgage.

The rampant price spikes of homes in most markets not only support the sale of the home to cure the delinquency, but also make mortgage modifications easier because many borrowers now have equity in their homes as a result of the home price gains.

Given the surge in home prices, a huge wave of foreclosures – as during the financial crisis – cannot happen. Home prices would have to fall broadly below mortgage balances before foreclosures become a mega-issue, which is what had happened in the run-up to the mortgage crisis.

How are FHA mortgages foreclosures doing?

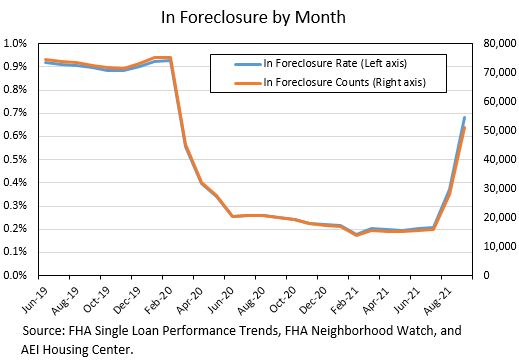

Foreclosures among FHA-insured mortgages surged in August and September following the end of the foreclosure moratorium on July 31, but they surged off the very low levels (in the 15,000 range) during the foreclosure moratorium. By the end of September, there were 50,910 FHA mortgages in foreclosure, according to the AEI Housing Center, but that was still below pre-pandemic levels of around 75,000 foreclosures.

The foreclosure rate tripled in two months, from 0.2% through July, to 0.7% at the end of September.

The trend shows that over the next few months, foreclosures will likely surge beyond the pre-pandemic levels but are not going to reach the mega-proportions during the Financial Crisis since home sales, after the price gains, provide a functional cure for most distressed homeowners.

But foreclosure rates vary dramatically by market. And some markets have far higher foreclosure rates than the national average of 0.7%.

The table shows the 15 metros with the highest foreclosure rates among FHA-backed mortgages at the end of September. It also shows the number of FHA mortgages in those metros, and the number of those mortgages that are in foreclosure (data via the AEI Housing Center):

| Metro, foreclosures in September | FHA count | # in fore-closure | % in fore-closure | |

| 1 | Tallahassee, Fl | 9,644 | 164 | 1.7% |

| 2 | Minneapolis-St. Paul-Bloomington, MN-WI | 77,943 | 1,246 | 1.6% |

| 3 | Chicago-Naperville-Evanston, Il | 171,768 | 2,669 | 1.6% |

| 4 | Albany-Schenectady-Troy, NY | 23,256 | 334 | 1.4% |

| 5 | Oklahoma City, OK | 50,738 | 722 | 1.4% |

| 6 | Syracuse, NY | 20,194 | 272 | 1.3% |

| 7 | Cleveland-Elyria, OH | 65,552 | 870 | 1.3% |

| 8 | Jacksonville, FL | 47,153 | 620 | 1.3% |

| 9 | Columbus, OH | 57,938 | 735 | 1.3% |

| 10 | Pensacola-Ferry Pass-Brent, FL | 12,741 | 159 | 1.2% |

| 11 | Tulsa, OK | 33,118 | 406 | 1.2% |

| 12 | Little Rock-North Little Rock-Conway, AR | 26,575 | 316 | 1.2% |

| 13 | Palm Bay-Melbourne-Titusville, FL | 17,004 | 201 | 1.2% |

| 14 | Indianapolis-Carmel-Anderson, IN | 77,024 | 892 | 1.2% |

| 15 | Akron, OH | 10,420 | 253 | 1.2% |

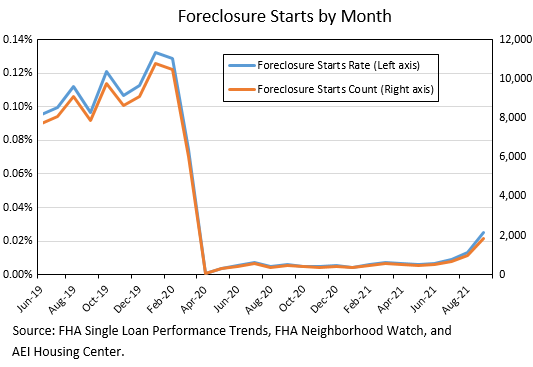

Foreclosure starts among FHA mortgages have also jumped, but from ultra-low levels during the foreclosure moratorium, to 2,000 starts in September, compared to the range of 10,000 starts before the pandemic.

So foreclosures will continue to surge as more FHA mortgages come to the end of their forbearance plans, but they’re surging from the historically low levels during the foreclosure moratorium, and given the massive amount of home-price inflation during the pandemic, are not going to build into the tsunami of foreclosures seen during the Financial Crisis.

This assumes that home prices in those markets don’t head south over the next 12 months.

The Fed engineered this home price inflation with its $4.5 trillion in asset purchases, including purchases of mortgage-backed securities, to repress long-term interest rates, including mortgage rates to record lows, thereby driving up prices. It also created an enormous amount of excess liquidity that needed a place to go, and some of it piled into the housing market, driving up prices. And the Fed thereby bailed out mortgage lenders and their guarantors once again.

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Classic Metal Roofing Systems, our sponsor, manufactures beautiful metal shingles:

- A variety of resin-based finishes

- Deep grooves for a high-end natural look

- Maintenance free – will not rust, crack, or rot

- Resists streaking and staining

Click here or call 1-800-543-8938 for details from the Classic Metal Roofing folks.

Read More:What’s Happening with the Massive Delinquencies of FHA High Risk & Subprime Mortgages Now that Foreclosure Bans Ended?

2021-11-08 04:24:38