But wait… Supply suddenly burst from the woodwork when mortgage rates surged before the Housing Bust. And for a reason.

By Wolf Richter for WOLF STREET.

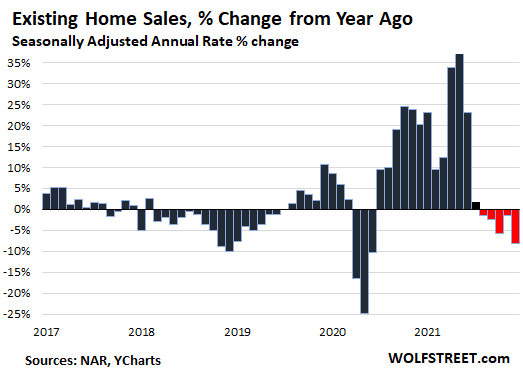

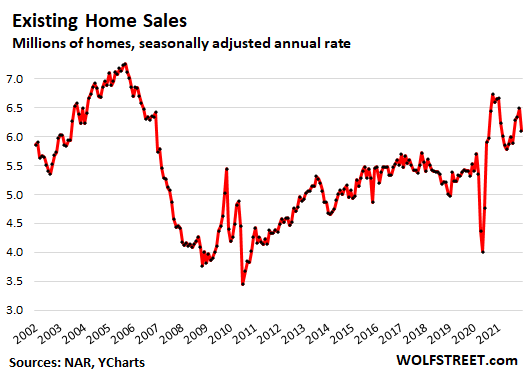

Sales of previously owned houses, condos, and co-ops in December fell by 4.6% month-to-month and by 8.3% year-over-year, to a seasonally adjusted annual rate of 6.1 million homes, the National Association of Realtors reported today. It was the fifth month in a row of year-over-year declines, amid very tight supply and rising mortgage rates (historic data via YCharts):

Seen over the long term, the seasonally adjusted annual rate of sales in December of 6.1 million homes wasn’t only below the peaks of 2020 but also well below the peaks during the 2003-2006 era.

Sales of single-family houses dropped 5.9% for the month and by 8.1% year-over-year, to a seasonally adjusted annual rate of 5.44 million houses.

Sales of condos plunged by 7.0% for the month and by 9.6% year-over-year to a seasonally adjusted annual rate of 660,000 condos.

By Region, the seasonally adjusted annual rate of total home sales dropped year-over-year in all four regions:

- Northeast: -15.7%

- Midwest: -2.6%

- South: -5.3%

- West: -10.2%.

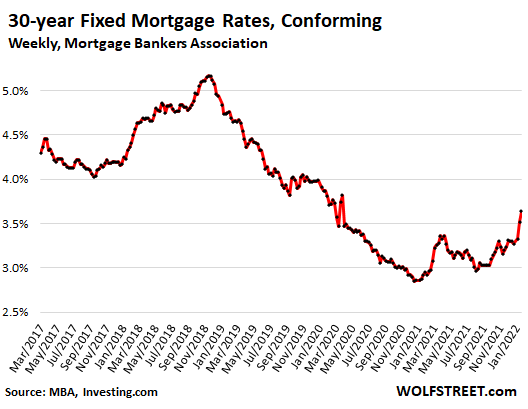

The scramble to lock in still low but spiking mortgage rates.

The average 30-year fixed rate of conforming mortgages in December was around 3.30%, which was up from November’s range of around 3.20%. But in January so far, mortgage rates have spiked. In the reporting week through January 19, the average 30-year fixed rate hit 3.64%, according the Mortgage Bankers Association (data via Investing.com):

The National Association of Realtors, back in its November report a month ago, expected the average 30-year mortgage rate to reach 3.70% by the end of 2022.

But the average daily 30-year fixed rate already kissed 3.70% on Wednesday, according to Mortgage News Daily data.

There are now two dynamics at play: As mortgage rates rise, more buyers are priced out, and they step away. But other buyers are accelerating their efforts to buy, no matter what the price, to lock in the still low mortgage rates.

“With mortgage rates expected to rise in 2022, it’s likely that a portion of December buyers were intent on avoiding the inevitable rate increases,” the NAR report said.

Buyers will do this until mortgage rates reach a magic level, at which point buyers begin to pull back. Mortgage rates beyond the magic level have the effect of cooling the housing market, which is what happened in the second half of 2018 and in 2005/2006.

Mortgage rates hit 5.0% in November 2018. And they hit 6.6% in the summer of 2006. And that was it for the housing market.

By the end of 2018, the stock market was in turmoil. The housing market was cooling off. All heck was breaking loose. And the Fed, which had been hiking rates and was reducing its balance sheet all year, was getting publicly hammered on a daily basis by President Trump.

At the time, inflation was right near the Fed’s target of 2.0% “core PCE.” So it in 2019, the Fed began signaling its infamous U-turn. It called off further rate hikes. By mid-2019, it ended its balance sheet reduction. In September 2019, it began bailing out the repo market that was blowing up.

Now it’s a different scenario: the worst inflation in 40 years.

In November, “core PCE” inflation hit 4.7%. The December “core PCE” inflation rate, to be released next week, will likely come in around 5.0%. And the Fed is starting to crack down on it – way too little, way too late, but it’s starting. So the Fed is unlikely to make a U-Turn while inflation is this red-hot.

Buying a home “now” to lock in a lower mortgage rate is a classic reaction to the initial phases of rising mortgage rates, also promoted by the real estate industry. It’s only when mortgage rates reach a magic pain level that sales volume dries up.

The NAR today also expressed this view that higher mortgage rates this year would hit the housing market and that existing-home sales would “slow slightly in the coming months due to higher mortgage rates.”

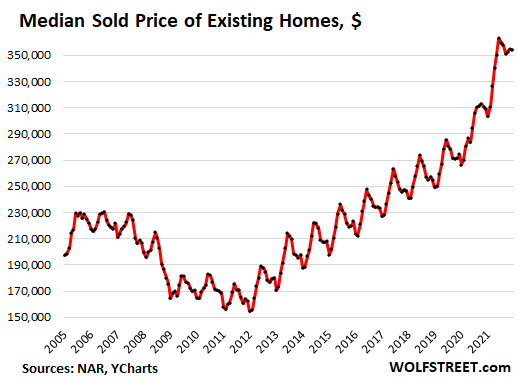

The median price spikes less.

At $354,300, the median price was unchanged for the month and was up 14.6% year-over-year. The year-over-year price spikes had peaked in May and June at over 23%. Since June, the median price has dipped 2.3%, a seasonal dip in the second half.

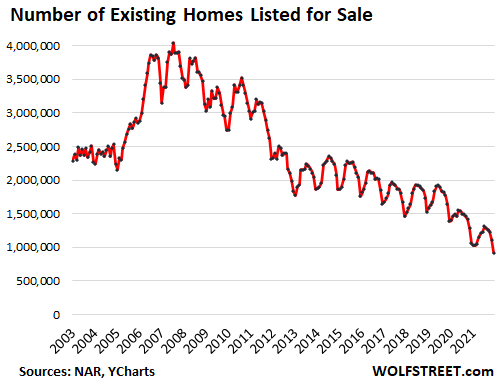

Supply of homes listed for sale declined to a record low of 1.8 months of sales. The number of unsold homes on the market declined to 920,000, seasonally adjusted.

But supply always comes out of the woodwork when interest rates rise and prices stall or decline. We saw that during the housing crash: All kinds of supply sudden hit the market, with investors that owned multiple homes being among the biggest group to just let the banks worry about those houses when buyers didn’t show up.

“Individual investors or second-home buyers, who make up many cash sales, purchased 17% of homes in December, up from 15% in November and up from 14% in December 2020,” according to the NAR.

Once homes are treated as investment products, like stocks, and not as homes, there can never be enough supply during a bull market. But when mortgage rates surge and when the market turns, those investors and second/third home buyers can easily put their vacant homes on the market — and they do. And suddenly, there’s supply coming out of the woodwork.

Note the storm surge of homes suddenly flooding the market in 2005 and 2006 as mortgage rates surged just ahead of the housing bust:

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Classic Metal Roofing Systems, our sponsor, manufactures beautiful metal shingles:

- A variety of resin-based finishes & colors

- Deep grooves for a high-end natural look

- Maintenance free – will not rust, crack, or rot

- Resists streaking and staining

To reach the Classic Metal Roofing folks, click here or call 1-800-543-8938

Read More:Big Drop in Home Sales, Surging Mortgage Rates, Tight Supply: The New Dynamics Shaping Up

2022-01-21 05:19:24